Attorney-Approved Florida Loan Agreement Template

Attorney-Approved Florida Loan Agreement Template

In Florida, a Loan Agreement form serves as a crucial document that outlines the terms and conditions of a loan between a lender and a borrower. This form typically includes essential details such as the loan amount, interest rate, repayment schedule, and any collateral involved. Additionally, it may specify the rights and responsibilities of both parties, ensuring clarity and reducing the potential for disputes. The agreement can cover various types of loans, including personal loans, business loans, and mortgages, each tailored to meet specific needs. Furthermore, it often includes provisions for default, prepayment, and dispute resolution, providing a comprehensive framework for the financial transaction. By formalizing the loan arrangement, this document helps protect the interests of both the lender and the borrower, making it an indispensable tool in financial dealings within the state.

When navigating the Florida Loan Agreement form, several important aspects should be kept in mind to ensure a smooth process. Here are five key takeaways:

By keeping these points in mind, individuals can better navigate the complexities of the Florida Loan Agreement form and foster a more transparent lending relationship.

When filling out the Florida Loan Agreement form, it's important to approach the task with care. Here are five essential dos and don'ts to keep in mind:

By following these guidelines, you can help ensure that your Loan Agreement form is filled out properly and efficiently.

When entering into a loan agreement in Florida, several additional forms and documents may be necessary to ensure clarity and protection for both parties involved. Understanding these documents can help facilitate a smoother transaction.

Having these documents prepared and understood can greatly enhance the loan process. They serve to protect both the lender and the borrower, ensuring that all parties are aware of their rights and obligations. Engaging with these forms thoughtfully can lead to a more successful financial arrangement.

Promissory Note Template California Word - Both parties are encouraged to retain a copy of the signed agreement.

When engaging in the sale or purchase of personal property, it's important to have the appropriate documentation in place. Utilizing a New York Bill of Sale ensures that the transaction is legally recognized and protects both parties involved. For those seeking a reliable template, Fast PDF Templates offers a convenient solution to create this essential document.

A Florida Loan Agreement is a legal document that outlines the terms and conditions under which one party lends money to another. It specifies details such as the loan amount, interest rate, repayment schedule, and any collateral involved. This agreement protects both the lender and the borrower by clearly defining their rights and obligations.

Anyone involved in a lending transaction should consider using a Loan Agreement. This includes:

A formal agreement helps prevent misunderstandings and provides legal recourse if necessary.

A comprehensive Loan Agreement should include the following key elements:

Including these details ensures clarity and reduces the risk of disputes.

While verbal agreements can be legally binding, having a Loan Agreement in writing is highly recommended. A written document provides clear evidence of the terms agreed upon. In case of a dispute, it serves as a crucial reference point for both parties.

Yes, you can customize a Loan Agreement to fit your specific needs. While there are standard templates available, it’s important to tailor the agreement to reflect the unique aspects of your transaction. Just ensure that all essential elements are included and comply with Florida laws.

If the borrower defaults, the lender has several options. These may include:

The Loan Agreement should outline the steps to take in case of default, providing clarity for both parties.

While it’s not mandatory to hire a lawyer, consulting one can be beneficial, especially for larger loans or complex agreements. A legal professional can ensure that the document complies with state laws and adequately protects your interests.

To enforce a Loan Agreement in Florida, you may need to file a lawsuit in civil court if the borrower fails to repay the loan as agreed. Having a written agreement makes it easier to prove your case. Ensure you keep copies of all relevant documents, including the signed agreement and any communication regarding the loan.

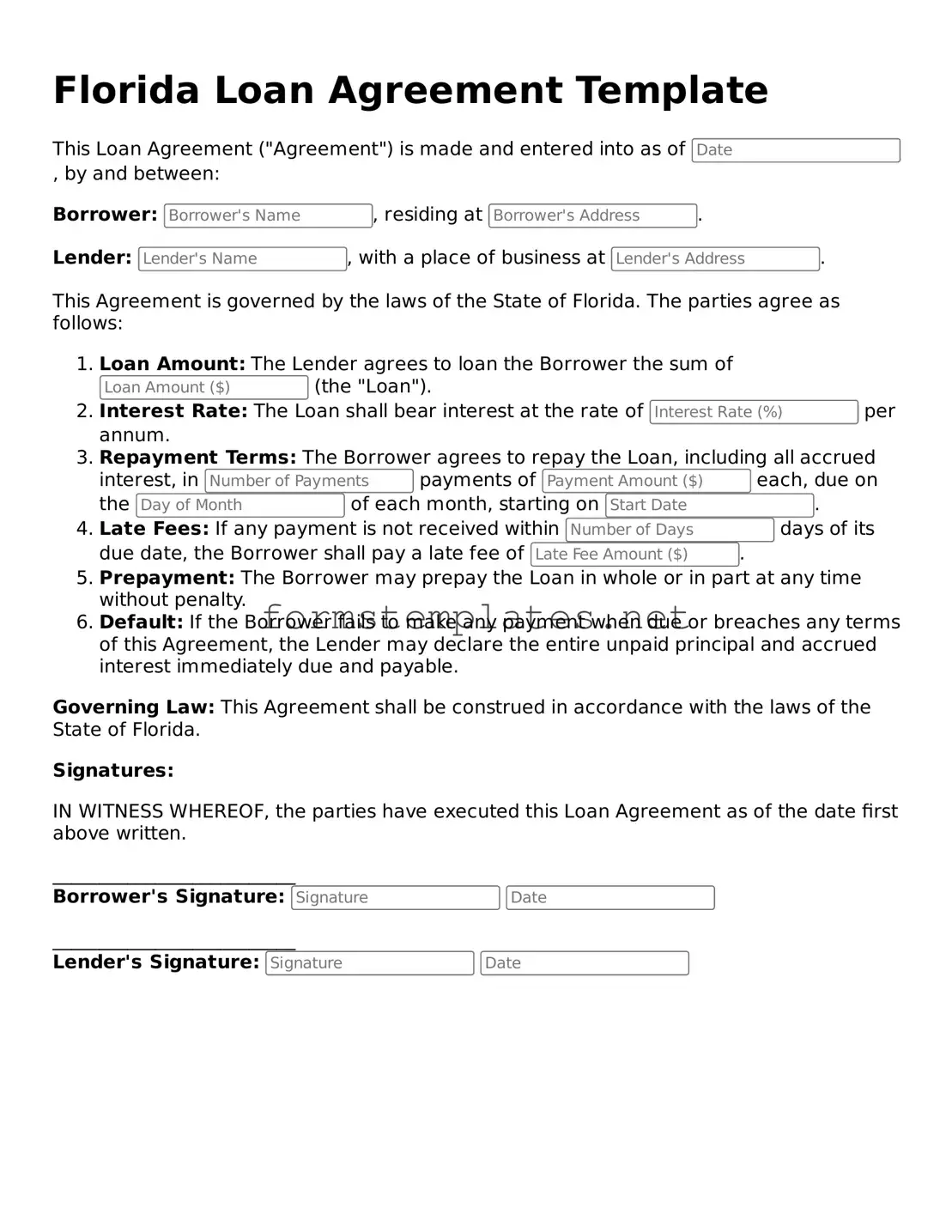

Florida Loan Agreement Template

This Loan Agreement ("Agreement") is made and entered into as of , by and between:

Borrower: , residing at .

Lender: , with a place of business at .

This Agreement is governed by the laws of the State of Florida. The parties agree as follows:

Governing Law: This Agreement shall be construed in accordance with the laws of the State of Florida.

Signatures:

IN WITNESS WHEREOF, the parties have executed this Loan Agreement as of the date first above written.

__________________________

Borrower's Signature:

__________________________

Lender's Signature:

| Fact Name | Details |

|---|---|

| Governing Law | The Florida Loan Agreement form is governed by the laws of the State of Florida. |

| Parties Involved | This form typically involves a lender and a borrower, clearly outlining their roles and responsibilities. |

| Interest Rates | The agreement specifies the interest rates applicable to the loan, which must comply with Florida's usury laws. |

| Default Provisions | It includes terms regarding default, detailing the actions that may be taken if the borrower fails to meet their obligations. |

After obtaining the Florida Loan Agreement form, you are ready to fill it out. This process involves providing specific information about the loan, the lender, and the borrower. Make sure to have all necessary details at hand before you begin.