Attorney-Verified Loan Agreement Form

Attorney-Verified Loan Agreement Form

A Loan Agreement form is a crucial document that outlines the terms and conditions of a loan between a lender and a borrower. It serves as a written record of the financial transaction, detailing essential aspects such as the loan amount, interest rate, repayment schedule, and any collateral involved. This form also specifies the rights and obligations of both parties, providing clarity on what is expected throughout the duration of the loan. It often includes provisions for default, outlining the consequences should the borrower fail to meet their repayment obligations. By establishing clear guidelines, the Loan Agreement form helps prevent misunderstandings and disputes, ensuring that both the lender and borrower are on the same page. Understanding this document is vital for anyone considering a loan, as it protects the interests of both parties and fosters a transparent lending process.

When filling out and using a Loan Agreement form, it is crucial to understand the following key points:

Understanding these elements can significantly enhance the effectiveness and clarity of a Loan Agreement.

When filling out a Loan Agreement form, it is important to follow certain guidelines to ensure accuracy and compliance. Here is a list of dos and don'ts:

A Loan Agreement is a crucial document that outlines the terms of a borrowing arrangement between a lender and a borrower. However, several other forms and documents often accompany this agreement to ensure clarity, compliance, and protection for both parties involved. Below is a list of commonly used documents related to loan agreements.

These documents collectively enhance the loan agreement by providing necessary details and protections for both the lender and borrower. Understanding each of these forms can help individuals navigate the borrowing process more effectively and ensure a smoother transaction.

Simple Hunting Lease Agreement Template - Requires lessee to report any property damage promptly.

For those seeking clarity in their business arrangements, our guide on the Illinois Operating Agreement is essential for understanding the roles within your LLC. You can find this vital document outlined in our detailed Illinois Operating Agreement instructions.

I9 Verification - Essential for any background investigation related to employment.

A Loan Agreement form is a legal document that outlines the terms and conditions of a loan between a borrower and a lender. It specifies the amount borrowed, the interest rate, the repayment schedule, and any collateral involved. This document serves to protect both parties by clearly defining their rights and responsibilities.

Anyone who is borrowing or lending money should consider using a Loan Agreement. This includes individuals, businesses, and organizations. A formal agreement helps prevent misunderstandings and provides a clear record of the transaction. Even informal loans between friends or family can benefit from a written agreement.

A comprehensive Loan Agreement typically includes the following key components:

Interest can be calculated in different ways, depending on the terms of the Loan Agreement. The most common methods include:

It’s essential to clarify how interest will be calculated in the agreement to avoid confusion later.

Yes, a Loan Agreement can be modified if both parties agree to the changes. It is advisable to document any modifications in writing and have both parties sign the amended agreement. This ensures that the new terms are clear and enforceable.

If the borrower defaults, the lender has specific rights as outlined in the Loan Agreement. These may include:

It's crucial for both parties to understand the default terms before entering into a Loan Agreement.

While it is not strictly necessary, having a lawyer review a Loan Agreement is highly recommended. A legal professional can ensure that the terms are fair, compliant with state laws, and protect your interests. This can be particularly important for larger loans or complex agreements.

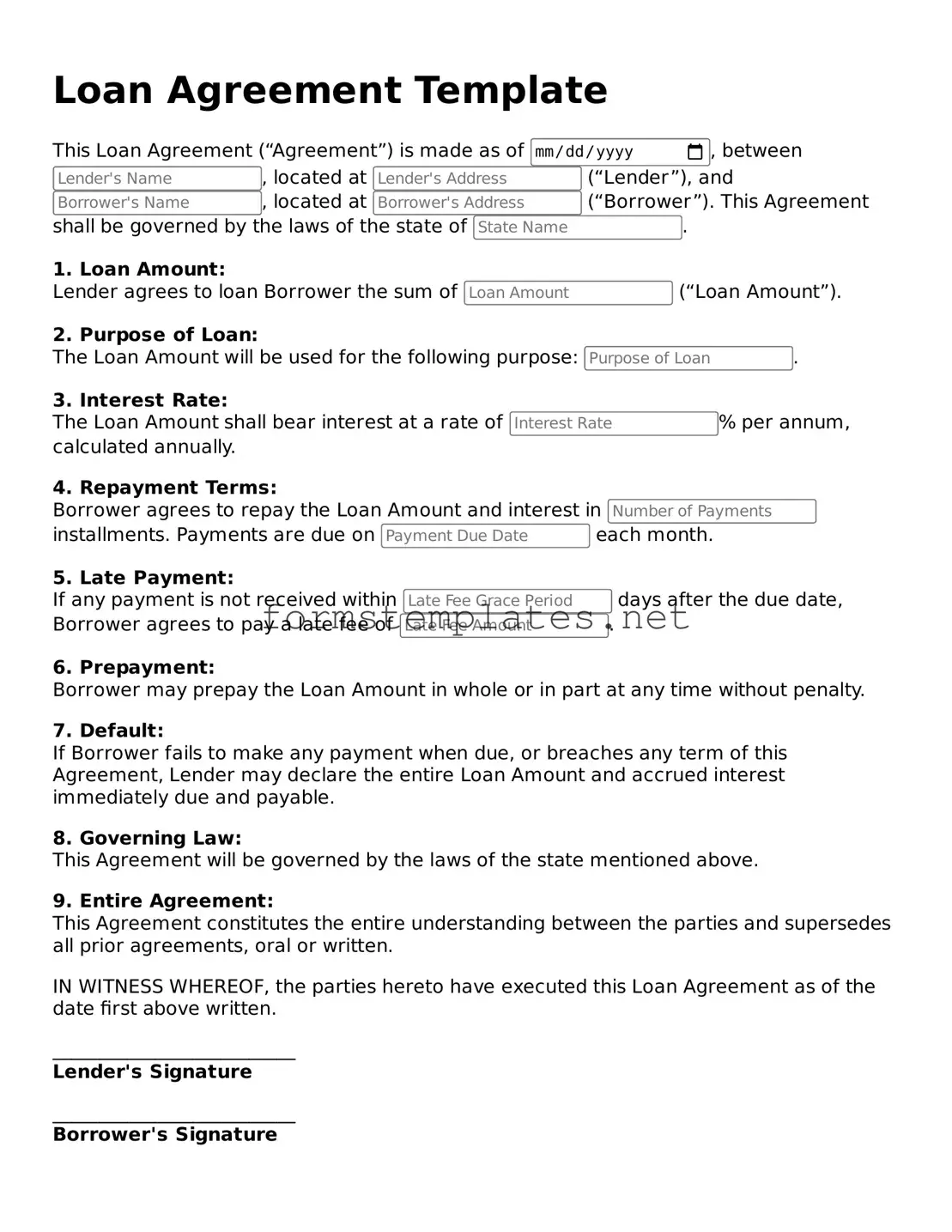

Loan Agreement Template

This Loan Agreement (“Agreement”) is made as of , between , located at (“Lender”), and , located at (“Borrower”). This Agreement shall be governed by the laws of the state of .

1. Loan Amount:

Lender agrees to loan Borrower the sum of (“Loan Amount”).

2. Purpose of Loan:

The Loan Amount will be used for the following purpose: .

3. Interest Rate:

The Loan Amount shall bear interest at a rate of % per annum, calculated annually.

4. Repayment Terms:

Borrower agrees to repay the Loan Amount and interest in installments. Payments are due on each month.

5. Late Payment:

If any payment is not received within days after the due date, Borrower agrees to pay a late fee of .

6. Prepayment:

Borrower may prepay the Loan Amount in whole or in part at any time without penalty.

7. Default:

If Borrower fails to make any payment when due, or breaches any term of this Agreement, Lender may declare the entire Loan Amount and accrued interest immediately due and payable.

8. Governing Law:

This Agreement will be governed by the laws of the state mentioned above.

9. Entire Agreement:

This Agreement constitutes the entire understanding between the parties and supersedes all prior agreements, oral or written.

IN WITNESS WHEREOF, the parties hereto have executed this Loan Agreement as of the date first above written.

__________________________

Lender's Signature

__________________________

Borrower's Signature

| Fact Name | Description |

|---|---|

| Purpose | A Loan Agreement form outlines the terms and conditions of a loan between a lender and a borrower. |

| Parties Involved | The form identifies the lender and the borrower, including their legal names and contact information. |

| Loan Amount | The specific amount of money being borrowed is clearly stated in the agreement. |

| Interest Rate | The form specifies the interest rate applied to the loan, which can be fixed or variable. |

| Governing Law | The Loan Agreement may be governed by the laws of a specific state, such as California or New York. |

| Repayment Terms | The repayment schedule, including due dates and payment methods, is detailed in the agreement. |

Filling out the Loan Agreement form is a crucial step in securing your loan. Completing this form accurately ensures that all parties understand the terms and conditions of the agreement. Below are the steps you should follow to fill out the form correctly.

Once you have completed the form, review it carefully for any errors or omissions. A well-filled form can expedite the loan approval process.