Free Profit And Loss Template

Free Profit And Loss Template

The Profit and Loss form, commonly referred to as the P&L statement, serves as a vital tool for businesses to assess their financial performance over a specific period. It provides a comprehensive overview of revenues, costs, and expenses, enabling stakeholders to gauge profitability. By detailing income generated from sales and subtracting the associated costs, the P&L form highlights net profit or loss. Key components include gross revenue, operating expenses, and net income, each playing a crucial role in understanding a company's financial health. This form not only aids in internal decision-making but also supports external reporting requirements, making it essential for investors, management, and regulatory bodies alike. Furthermore, the P&L statement can reveal trends over time, helping businesses strategize for future growth and sustainability.

Understanding how to fill out and utilize a Profit and Loss form is essential for anyone managing a business. Here are some key takeaways to keep in mind:

By keeping these points in mind, you can maximize the effectiveness of your Profit and Loss form and enhance your business's financial management.

When filling out the Profit and Loss form, it is important to follow certain guidelines to ensure accuracy and compliance. Here are six things you should and shouldn't do:

The Profit and Loss form is an essential document for understanding a business's financial performance over a specific period. However, several other forms and documents complement this form, providing a more comprehensive view of a company's financial health. Below are five important documents that are often used alongside the Profit and Loss form.

Using these documents together with the Profit and Loss form allows business owners and stakeholders to gain a clearer understanding of financial performance and make informed decisions. Each document plays a vital role in painting a complete picture of the business's financial health.

Shower Sheet - Prioritize skin assessments, as they are vital to the health of residents.

A Release of Liability form is a legal document that releases one party from responsibility for certain risks or injuries that may occur. It is often used in activities where there is a chance of injury, such as sports or recreational events. Understanding this form is important for both organizers and participants to ensure clear communication about potential risks. For more information and templates, you can visit Fast PDF Templates.

Form 680 - All doses must be listed in a specific order on the form.

The Profit and Loss form is a financial document that summarizes the revenues, costs, and expenses incurred during a specific period. It provides a clear overview of a business's financial performance, showing whether the company has made a profit or suffered a loss during that timeframe.

This form is crucial for several reasons:

The frequency of completing a Profit and Loss form can vary based on the needs of the business. Common practices include:

Ultimately, the choice depends on the size and complexity of the business.

A standard Profit and Loss form includes the following sections:

Analyzing the Profit and Loss form can reveal valuable insights. Here are some ways to utilize this information:

By regularly reviewing this form, businesses can adapt strategies to enhance overall performance.

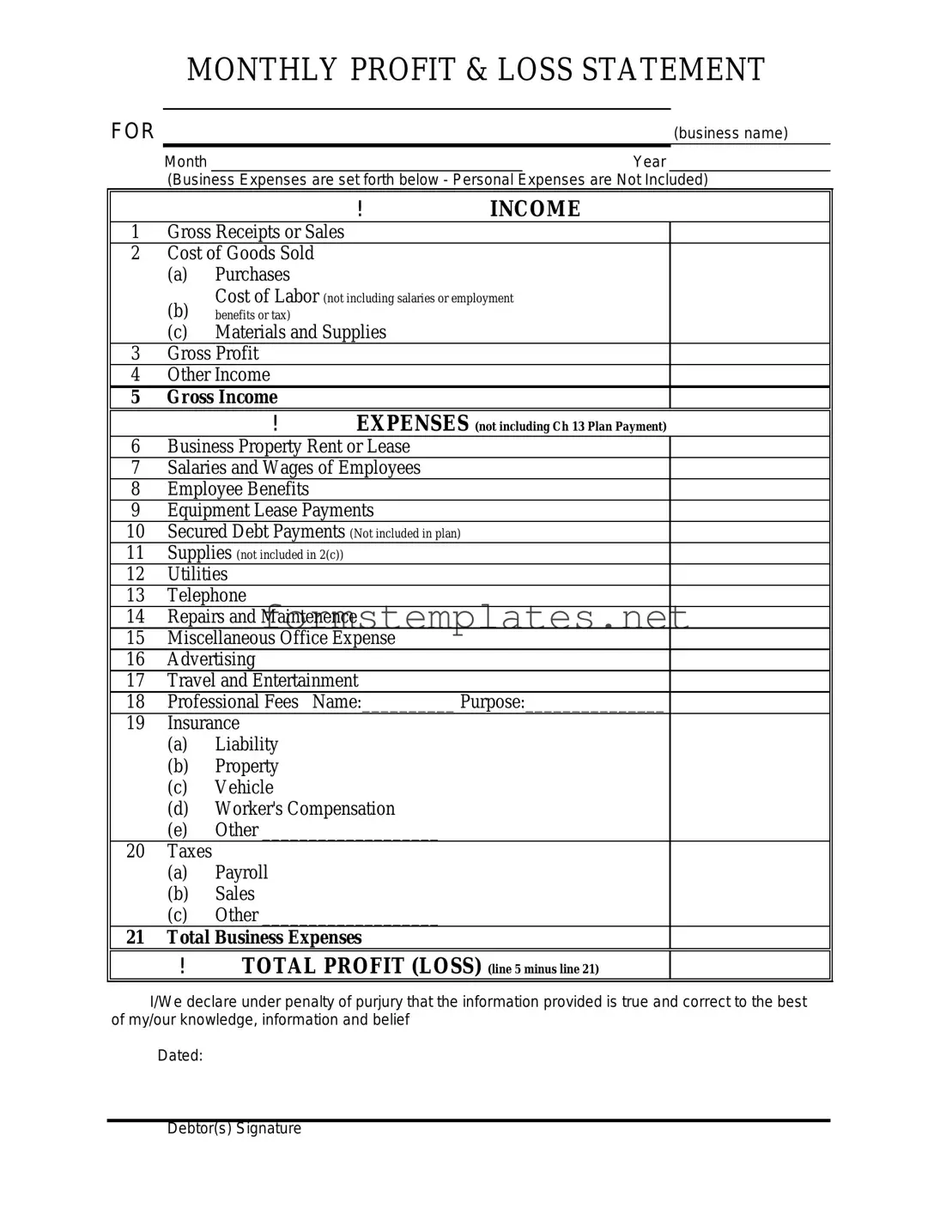

MONTHLY PROFIT & LOSS STATEMENT

FOR |

(business name) |

Month |

Year |

(Business Expenses are set forth below - Personal Expenses are Not Included)

|

|

|

! |

INCOME |

1 |

Gross Receipts or Sales |

|

||

2 |

Cost of Goods Sold |

|

||

|

(a) |

Purchases |

|

|

|

(b) |

Cost of Labor (not including salaries or employment |

||

|

benefits or tax) |

|

|

|

|

(c) |

Materials and Supplies |

|

|

3 |

Gross Profit |

|

|

|

4 |

Other Income |

|

|

|

5 |

Gross Income |

EXPENSES (not including Ch 13 Plan Payment) |

||

|

|

! |

||

6 |

Business Property Rent or Lease |

|

||

7 |

Salaries and Wages of Employees |

|

||

8 |

Employee Benefits |

|

|

|

9 |

Equipment Lease Payments |

|

||

10 |

Secured Debt Payments (Not included in plan) |

|

||

11 |

Supplies (not included in 2(c)) |

|

||

12 |

Utilities |

|

|

|

13 |

Telephone |

|

|

|

14 |

Repairs and Maintenence |

|

||

15 |

Miscellaneous Office Expense |

|

||

16 |

Advertising |

|

|

|

17 |

Travel and Entertainment |

|

||

18 |

Professional Fees |

Name:__________ Purpose:_______________ |

||

19 |

Insurance |

|

|

|

|

(a) |

Liability |

|

|

|

(b) |

Property |

|

|

|

(c) |

Vehicle |

|

|

|

(d) |

Worker's Compensation |

|

|

|

(e) |

Other ___________________ |

|

|

20 |

Taxes |

|

|

|

|

(a) |

Payroll |

|

|

|

(b) |

Sales |

|

|

|

(c) |

Other ___________________ |

|

|

21 |

Total Business Expenses |

|

||

|

! |

TOTAL PROFIT (LOSS) (line 5 minus line 21) |

||

I/We declare under penalty of purjury that the information provided is true and correct to the best of my/our knowledge, information and belief

Dated:

Debtor(s) Signature

| Fact Name | Description |

|---|---|

| Definition | The Profit and Loss form summarizes a business's revenues and expenses over a specific period. |

| Purpose | This form is used to assess financial performance and determine profitability. |

| Key Components | Includes total revenue, cost of goods sold, gross profit, operating expenses, and net income. |

| Frequency | Typically prepared monthly, quarterly, or annually, depending on business needs. |

| Tax Implications | Used for tax reporting purposes, impacting income tax calculations. |

| State-Specific Forms | Some states require specific formats or additional disclosures based on local laws. |

| Governing Laws | In California, for example, the form must comply with the California Corporations Code. |

Filling out the Profit and Loss form is an important step in tracking your business's financial performance. By accurately completing this form, you can gain insights into your revenue and expenses, which can help inform future decisions. Follow the steps below to ensure you fill out the form correctly.